KFP Market View in September 2020

It’s different this time...

The US Federal Reserve launched a revolution at its annual Central Bankers’ summit on Thursday. Hard inflation targeting of 2%, which was the bedrock of US (and global) monetary policy since the late 1990’s, has been abandoned along with the Philips Curve on the relationship between employment and inflation. In its place is an innocuous sounding “average inflation of 2%” over a cycle…hardly revolutionary sounding, but the implications are profound.

The WSJ headline proclaimed “Low rates forever!”. In effect, the Fed has given itself license to ignore current inflation above the 2% level and maintain low real rates. As long as its self-defined average is not above 2%, the Fed will not raise rates, as opposed to the previous regime of almost automatic raising of interest rates as inflation approached 2%.

While paying lip service to inflation targeting of 2%, in practice the Fed could let inflation rise to significantly higher levels without taking action on interest rates. To add further to the uncertainty, the Fed has not spelt out how and over what period it will calculate the average – giving it, and its political masters, almost unlimited flexibility.

Why has the Fed made this 180 degree change? It is an attempt to boost the growth recovery AND generate higher levels of inflation through negative real interest rates, all designed to erode the real debt burden of the US. Without inflation to do the heavy lifting, US (and other countries’) debt levels will continue to rise in real terms and ultimately become unsustainable.

Paul Volcker will be turning in his grave.

Inflation on the horizon

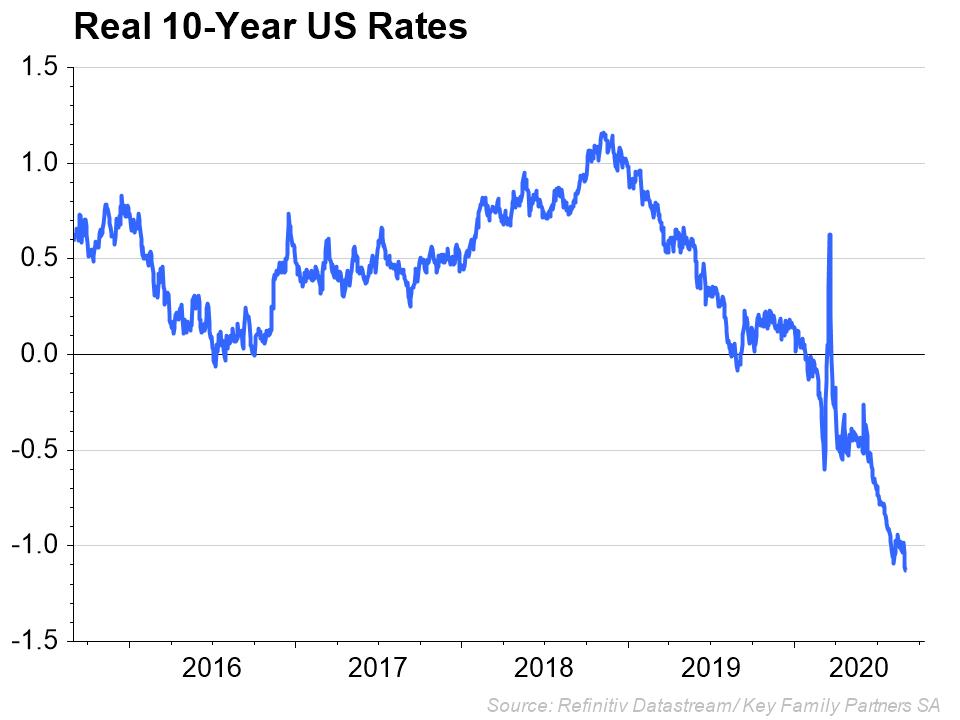

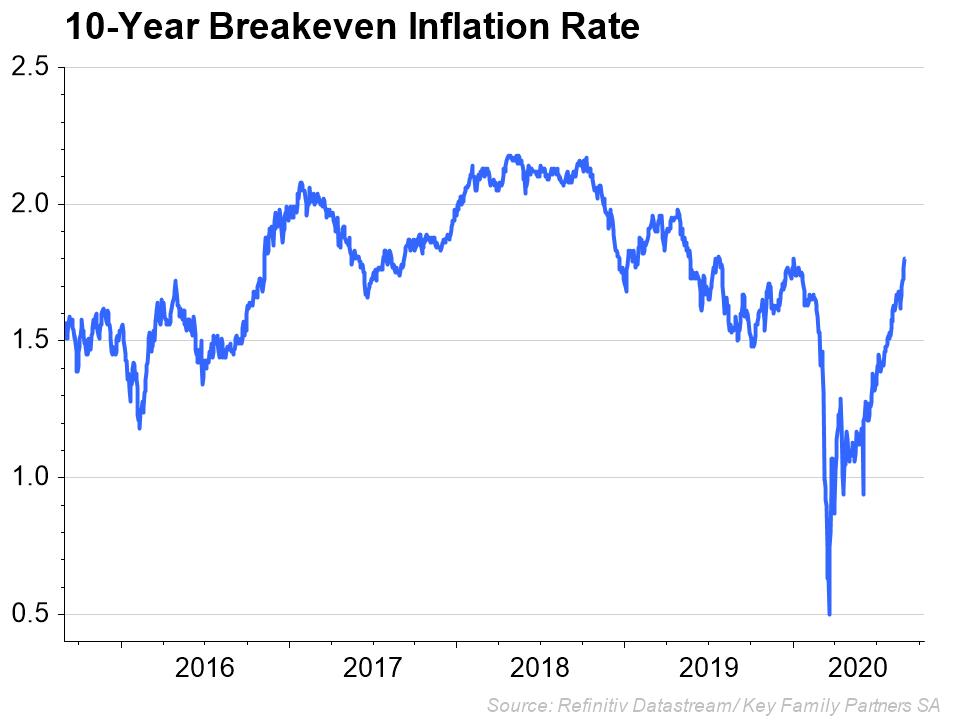

Meanwhile longer- term inflation expectations accelerated on the news, and real rates remained strongly negative.

10 year inflation expectations rose to levels last seen in December 2019 before the pandemic struck, and now have entered a rising trend rather than falling trend as was the case last December. The rise in inflation expectations from the lows in March of 124bps is the largest since the GFC in 2009/10, when inflationary conditions were higher at the start of the crisis than this time around.

Real 10 year rates have therefore fallen to the lowest seen this century, at -1.03%, suggesting that real interest rates will remain negative for a significant period of time. The trend for real rates remains strongly negative, implying we could see even more negative rates as inflation expectations rise and treasury yields remain pegged for the time being by Fed QE activity.

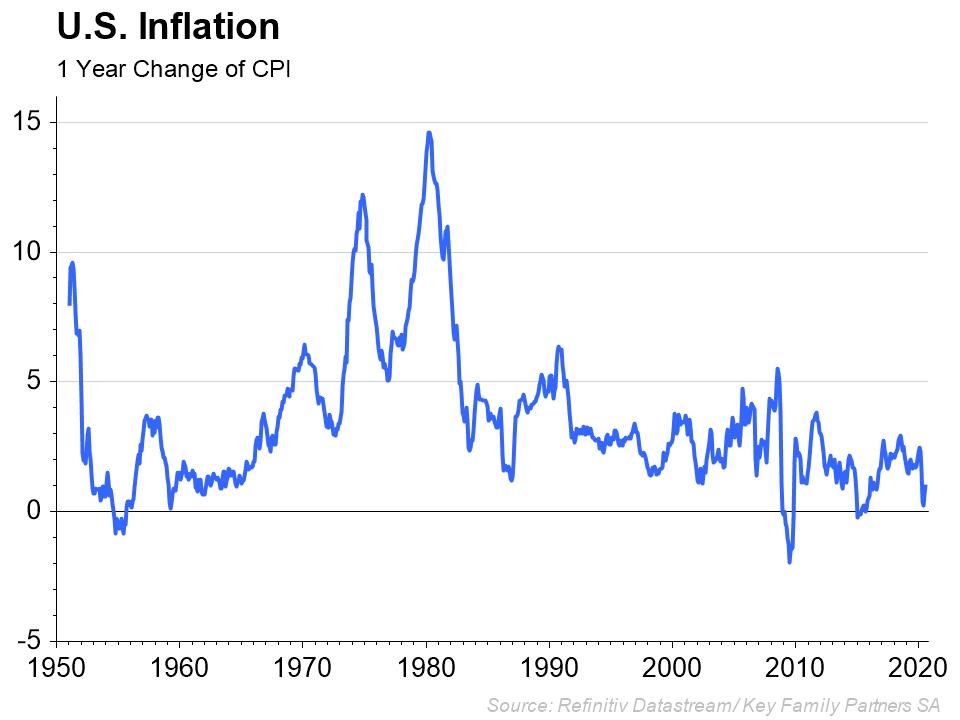

After 40 years of benign and falling inflation, is the inflation trend ready to reverse, and if so why? The long-term chart below suggests that inflation is set to rise longer term.

Many reasons have been given for the past 40 years of low inflation the world has experience. My view is that a perfect combination of trade liberalisation (including China joining the WTO with low cost manufactured goods), technology driven productivity, demographics and positive real interest rates kept inflation under control on a global scale during that period.

- Trade liberalisation has come to a halt. On the contrary, new tariff and non-tariff restrictions by major trading blocks are likely to increase prices of traded goods

- Productivity growth has slowed as the early rate of productivity gains from technology have slowed

- Most importantly, real interest rates have collapsed to negative levels in all developed markets, and zero in China

- Fiscal stimulus at extreme levels following the recent recession

Recent data suggests inflation rates are picking up in most DM and EM countries following the recession. However, many commentators have cited the example of Japan, which in spite of many years of zero interest rate policy and fiscal stimulus, has not succeeded in generating their target inflation level. I would give two reasons for this experience:

1) the world as a whole was in a low inflation environment as described above, from which Japan on its own could not escape, and in addition 2) Japan has the most most acute demographic challenge of any advanced economy, with an aging and shrinking population which is deflationary on a domestic level. If the level of global inflation is seen to rise, Japan may have more chance of achieving its own target levels and inflating away its large mountain of debt but the demographic challenge will remain.

How is the economic recovery going?

After the well documented recession in Q1&2, economic activity appears to be picking up across the world economy, but at very different rates. Differing monetary and fiscal policies, and approach to Covid lock downs, will explain most of the differences.

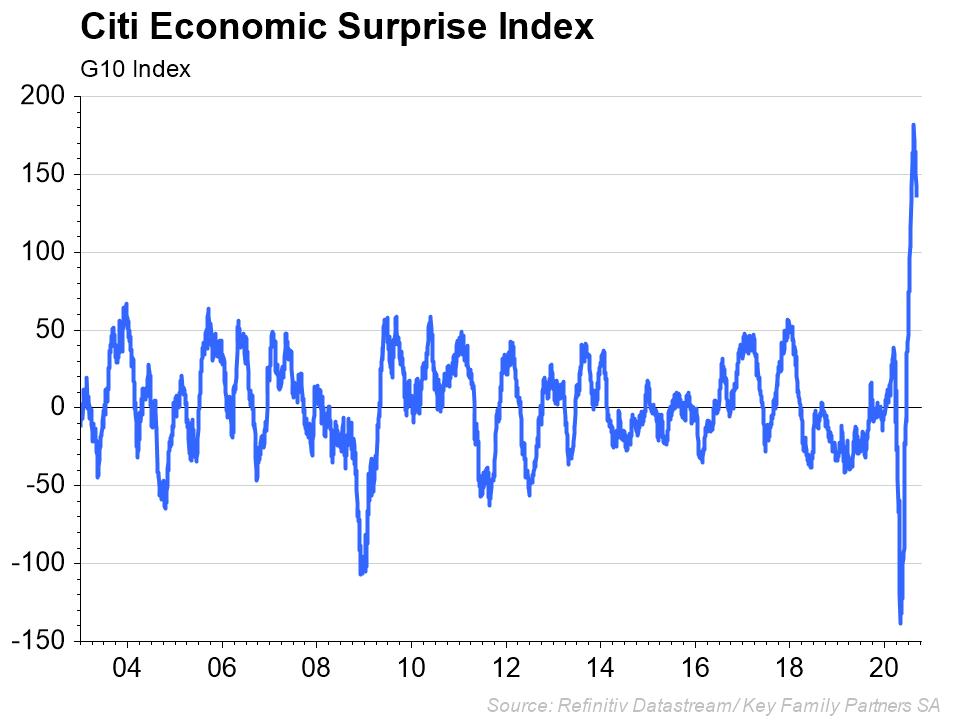

At a global level, using the Citi Economic Surprise index, the recovery is doing much better than expected in most countries. The question then becomes at what rate will economies recover from the record falls in GDP seen in the first half. For eg, the UK saw a 21.7% fall in GDP in the first half of 2020, but is now showing some rebound as lock down is eased.

This chart shows the dispersion of recovery levels experienced by different countries using some alternative real time measures such as credit card usage, and their economic activity relative to where they were at the start of 2020. Clearly, economic activity remains well below the start of the year but in most cases is recovering – except where new Covid outbreaks force renewed lock down as in South Korea.

China remains a standout post Covid performer, with manufacturing and non-manufacturing PMIs remaining in positive territory again in August – for the 6th consecutive month. China’s stated GDP growth year on year to June 30th stands at +3.2%, while every other major economy is in negative territory.

To summarise

- The world economy continues to recover, albeit at uneven and disparate rates. However, aggregate economic activity remains well below the start of the year, except in china

- The Fed has implemented a radical new monetary regime to attempt to boost recovery and inflation, leading to negative real rates for the foreseeable future

- Current inflation has stated to edge up, and longer term expectations have risen strongly

Investment implications

The implications of the Fed’s actions are profound:

- With rising inflation risk, fixed income instruments, particularly DM Government bonds, no longer represent the risk free default holdings to diversify away equity market risk

- Equities with growth potential and pricing power will be discounted at lower rates for longer and could go higher, while companies with low growth and pricing power will remain “cheap” (zombies)

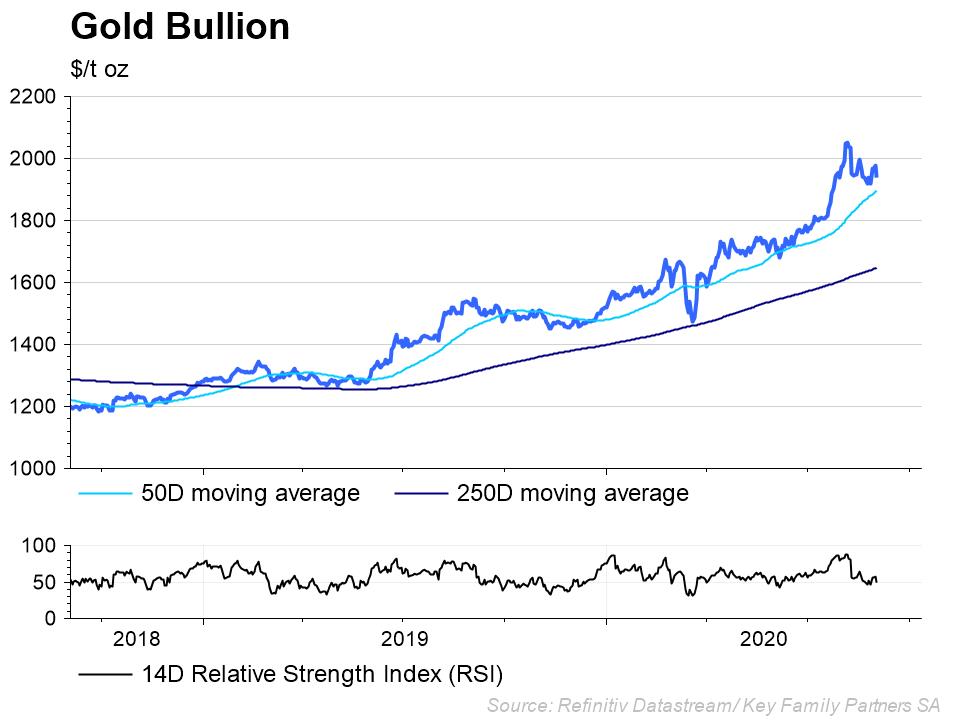

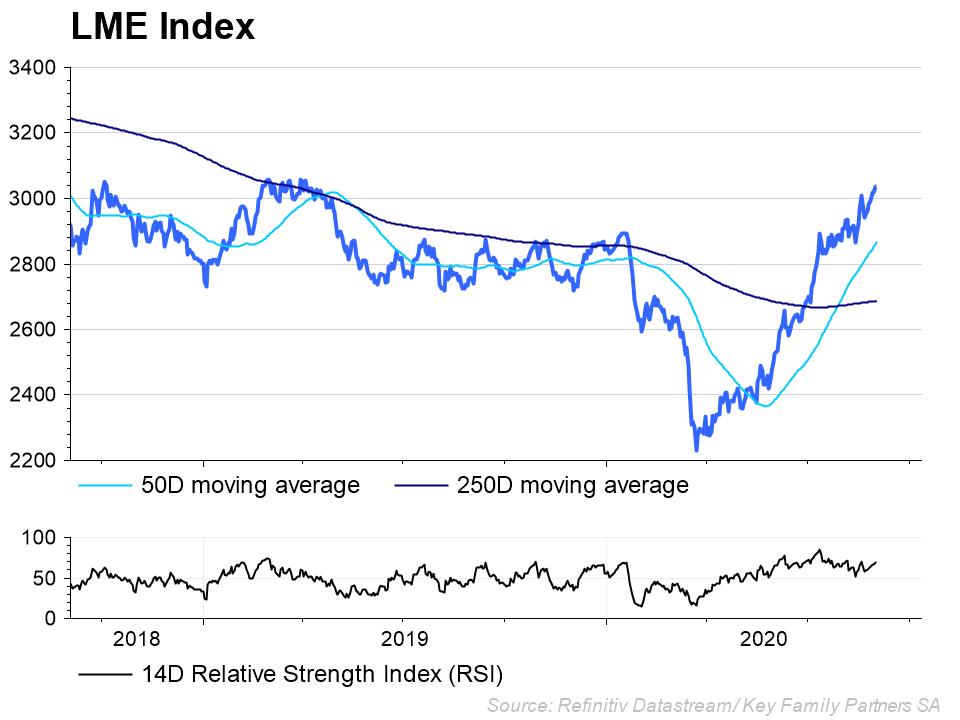

- Other assets (gold, real assets (eg base metals, lumber), some real estate) will provide diversification opportunities for investment portfolios

Portfolio rebalancing should be a priority for investors at this time.

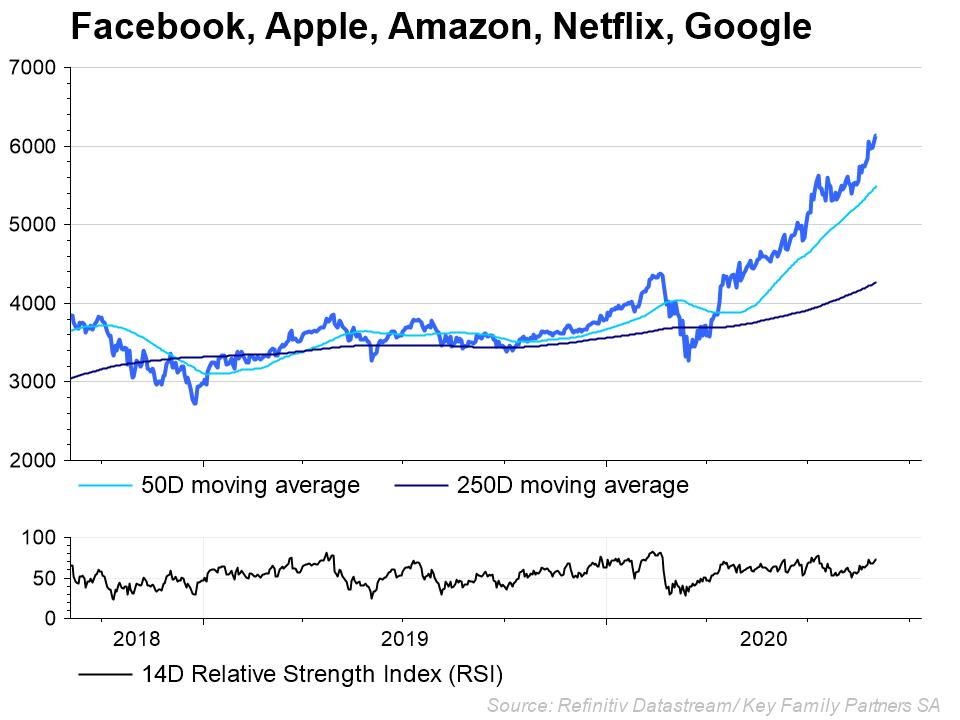

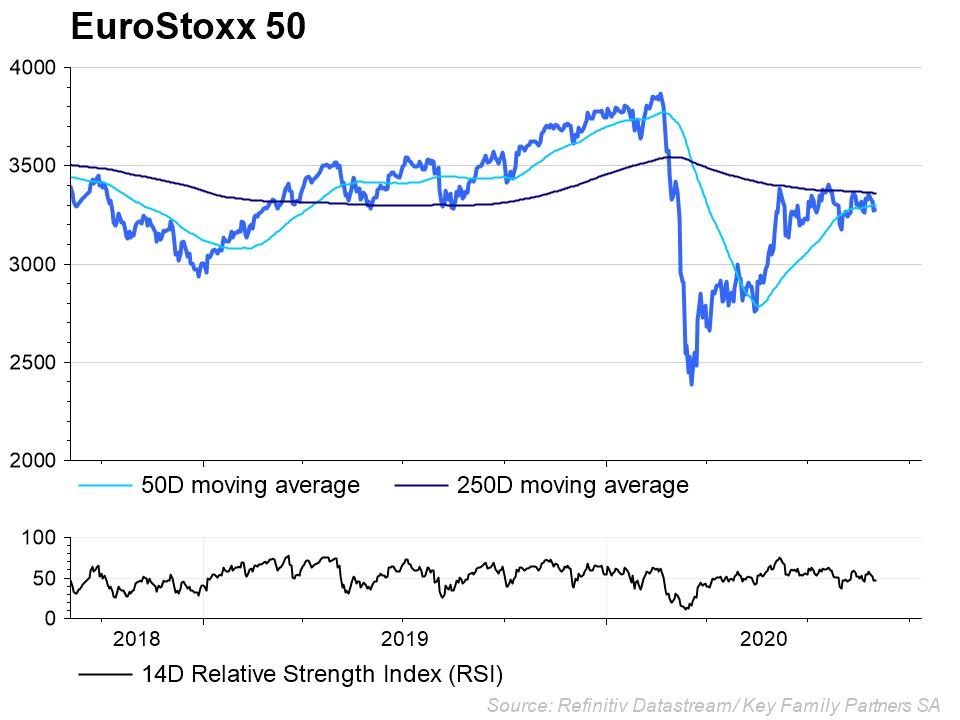

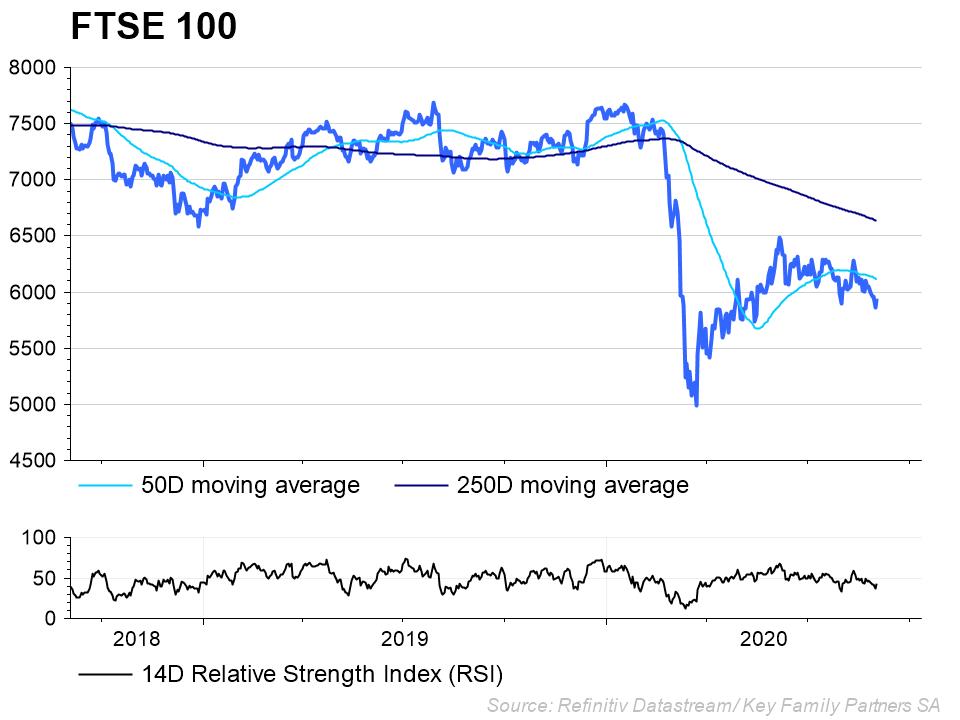

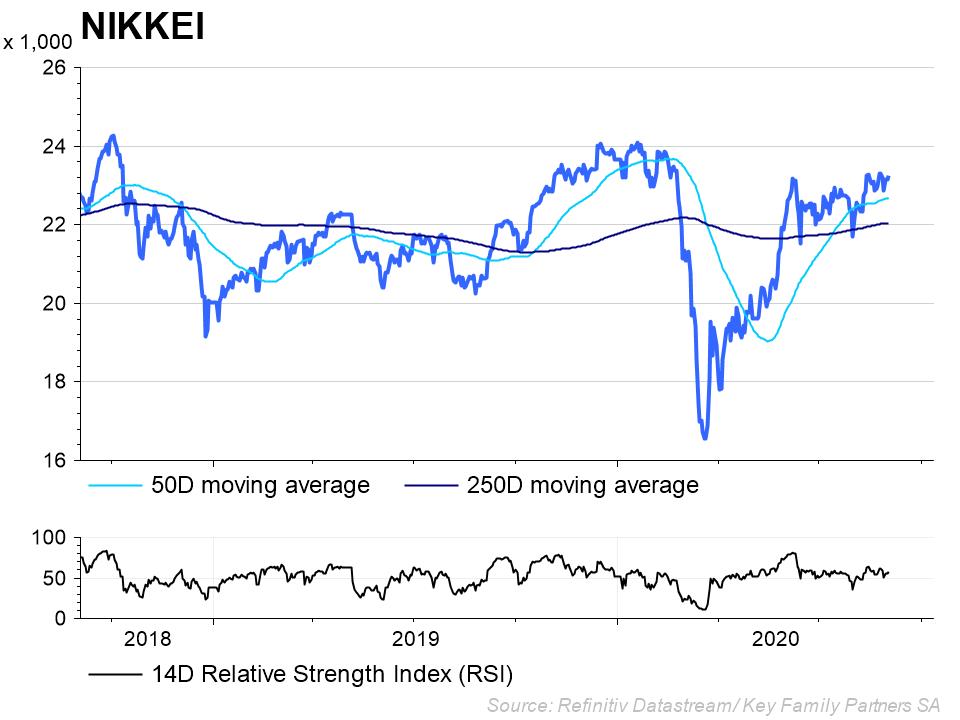

For more detailed commentary on each major market or asset class. Download the full Monthly Market View here.

Key Family Partners SA is a multi-family office based in Geneva, Switzerland. We serve our members with investment services, financial planning, administration, succession planning, education and philanthropy. Contact us at KFP@keyfamilypartners.com ~ +41 22 339 00 00 ~ Rue François-Bonivard 6, 1201 Geneva. https://www.keyfamilypartners.com/

This article may contain confidential and proprietary information. Any unauthorised disclosure, copying, storage or use of this presentation may be unlawful. The content of this presentation does not constitute investment or financial advice and may not be relied upon as such. It does not constitute an offer or invitation for the sale or purchase of services or securities and shall not form the basis of any contract. Key Family Partners SA does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Key Family Partners SA is a private limited company with its registered office at Rue François-Bonivard 6, 1201 Geneva, registered with the commercial registry of Geneva under the IDE Nr. CH-395.573.747. KFP is a member of the Swiss Association of Asset Managers (SAAM).